How To Pay Withholding Tax Tanzania

It is a withholding tax on taxable incomes of employees. The firm is supposed to pay tax.

C A June 2019 Tanzania Tax Update By Bcassian Issuu

The Act offers guidance with regards to what is sourced from Tanzania and section 69i provides.

How to pay withholding tax tanzania. The non-resident recipient must own at least 25 of the share capital of the capital of the Zambian company. Where a dividend is paid by a resident corporation to another resident corporation holding 25 or more of shares and voting rights in the corporation paying the dividend the WHT. Companies or entities have to prepare final accounts which must be approved by authorized Auditors and Accountants recognized by both NBAA and TRA.

Non-residents are taxable on income with a source in Tanzania. A Withholdee is a person liable to pay tax from the total income or final withholding payment. These accounts are submitted to TRA on the prescribed accounting date.

If it pays interest to any other recipient it must withhold tax at a rate of 10. Obligation to withhold tax. All companies whether resident or non-resident are required by the Income Tax laws to file an estimate of income within three months after the start of its accounting year.

Subject to tax when sourced from Tanzania. If these are sourced from Tanzania the withholding tax mechanism then kicks in to require the person making payment to collect tax at the point of payment. If your business pays interest to a resident financial institution there is no withholding tax.

Businesses in Tanzania are required to withhold tax on various payments including payments for service fees to nonresident service providers. This follows the decision of the Court of Appeal that on Friday upheld two previous decisions that rejected the companys. For an employee who makes a donation as per section 12 of education fund Act 2001 such donation is exempted from tax.

Upstream oil and gas exploration company Ophir Tanzania Block 1 Limited is to pay the Tanzania Revenue Authority TRA Sh183 billion after losing a legal battle to challenge the tax liability imposed on it in 2014. It includes a permanent employee part time manager director and. The rate of 5 shall apply where the beneficial owner is a company that directly holds at least 10 of the capital of the company paying the dividends or.

The normal rate of WHT on dividends is 10. The amendments further propose timing of the withholding tax on the employment income to be the time of selling minerals and payment of royalty. Under this system tax payable is established based annual turnover shown by taxpayers records.

Ii Computation and payment of withholding taxes is done online through wwwtragotz iii The submission of statement is within 30 days after each 6- month period. An employee means an individual who is a subject of an employment conducted by an employer. This is a tax which is paid from corporate profits.

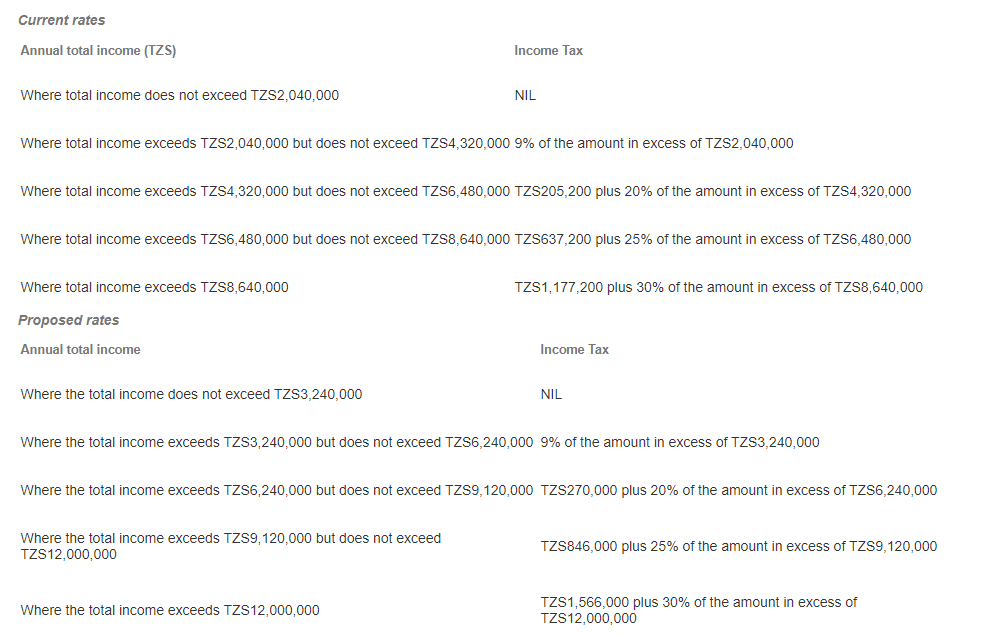

50 Resident Individual Income Tax Tanzania Mainland Monthly Income Tax Rate. Effecting payments to employees. If the recipient is non-resident the tax is final.

Preparation of monthly payroll completion of relevant monthly and annual forms monitoring effecting statutory payments. Assistance with payment and filing of other tax returns VAT withholding tax. The individuals income for any year must consist exclusively of income from business with sources in the United Republic of Tanzania.

Withholding Tax Statement-a payments made by the withholding. Prior to July 2016 withholding tax WHT only applied to such payments either where services were rendered in Tanzania or where the payer for the services was the Government of Tanzania then irrespective of place of performance. And any other information that the Commissioner may prescribe.

The lower rate applies if the beneficial owner is a company that controls directly or indirectly at least 15 of the voting power in the company paying. In absence of complete records annual turnover will be estimated based on the best judgment of the commissioner. Income tax is charged at a rate of 30 on income of a resident corporation and of a permanent establishment PE of a non-resident corporation or 5 of turnover for technical and management service providers to mining oil and gas entities deducted by way of WHT.

Dividend payments are taxed by way of WHT and this is a final tax. So where the payer was not the Government the question was whether services had been rendered in Tanzania. The domestic WHT rate applies unless the DTT rate is lower in which case the lower DTT rate applies.

The turnover bands and their tax. Rates of tax under presumptive tax System. I Payment of withholding taxes should be within 7 days after the month of deduction.

Under this system an employer is required by law to deduct income tax from an employees taxable salary or wages. PAYE stands for Pay-As-You-Earn. The withholdee of a payment that is not a final withholding payment shall be entitled to a tax credit in an amount equal to the tax treated as paid for the year of income in which the payment is derived.

If the recipient is resident the tax is non-final. Engaged in small scale mining operations to pay withholding tax at a rate of 06 percent in relation to employment income of an employee to that individual. Filing of Withholding tax statements Every withholding agent shall file with the Commissioner General within 30 days after the end of each 6-month calendar period a statement of any income tax withheld during the month by filling the prescribed form ITX 23001E.

That is what the law provides. For non-resident employees of a resident employer the income subject to withholding tax is the total income of a non-resident individual and is charged at a rate of 30. Tax Credit for non-final withholding tax Section 87 of ITA.

Processing annual tax clearance. Every withholding agent shall file with the Commissioner within 30 days after the end of each six-month calendar period a statement in the manner and form prescribed specifying payments made by the agent during the period that are subject to withholding tax the name and address of the withholdee income tax withheld from each payment.

The Income Tax Act Tanzania Investment Centre

Tanzania Individual Summary

In Review Direct Taxation Of Businesses In Tanzania Lexology

Tanzania Vs African Barrick Gold Plc August 2020 Court Of Appeal Case No 144 Of 2018 2020 Tzca 1754 Tpcases Com

Tenmet Human Resources Administrative Manual Tanzania

Chapter 332 The Income Tax Act Tanzania Revenue Free Download Pdf

Tanzania S Parliament Passes Finance Bill 2020 Ey Global

Taxation In Tanzania Cdr Tanzania Investment Forum

Assad Associates Live Tra E Filing Seminar Facebook

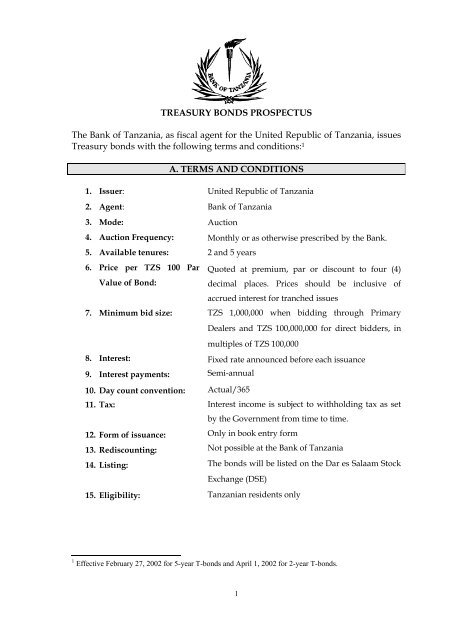

Treasury Bonds Prospectus Bank Of Tanzania

Tanzania Revenue Authority Paye Slab Tra Paye Lenvica Hrms

Tanzania In Imf Staff Country Reports Volume 1998 Issue 005 1998

Tanzania Finance Act 2019 Activpayroll

Http Www Un Org Esa Ffd Wp Content Uploads 2014 11 10stm Presentationbajungu Pdf

Pin On Teaching Social Studies

Tanzania Revenue Authority Ppt Download

Compliance Calendar Tanzania Secretarial Taxation Hr Labour Ehs

Tanzania Revenue Authority Paye Slab Tra Paye Lenvica Hrms

Https Www2 Deloitte Com Content Dam Deloitte Tz Documents About Deloitte Covid 19 20tanzania 20tax 20 20legal 20viewpoint Pdf

{kind=link}

Post a Comment for "How To Pay Withholding Tax Tanzania"